Hi! Today, I’m going a little bigger picture to discuss the evolution of yield farming and digital income. Markets-wise, I’m still bearish crypto. I promise you I’m not a permabear, though I have been bearish since November for piles of reasons all outlined in MTC #4 through #8. My four main conditions for turning bullish are in MTC #11: Sober.

A cat that reminds me of Deadmau5

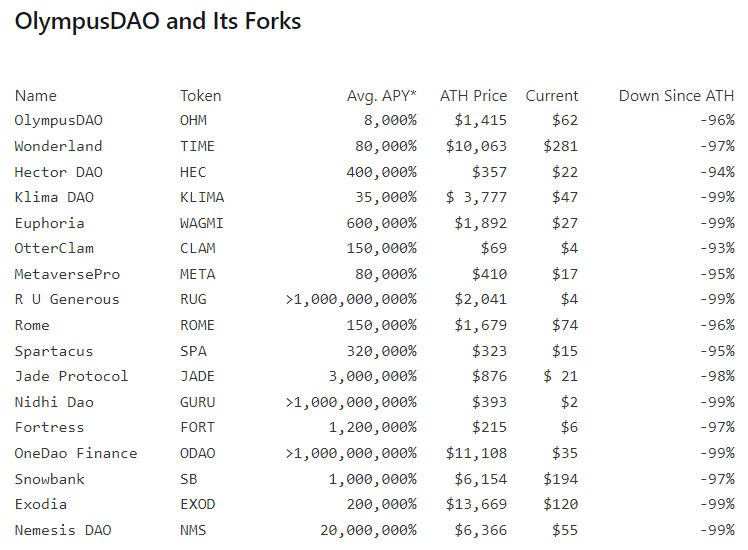

Many in traditional finance look at DeFi, staking, and yield farming and see something that is obviously making promises that cannot be kept. For example, the infamous but not particularly unique Defi Wonderland.

Eighty-thousand percent! That seems pretty good. :U

Any rational actor who has taken a corporate finance class or whatever would be thinking: There must be earthquake-style risk of ruin here to compensate for that Martian level of yield.

For perspective, here is a chart of Wonderland’s annual percentage yield (APY) vs. a TradFi banking system APY:

Wonderland APY vs. Marcus Online Savings by Goldman Sachs APY

And the Marcus by Goldman Sachs website tells me their APY is 4X the national average!

Sidenote: “Marcus by Goldman Sachs” ranks up there with “Ruth’s Chris Steak House” and “Duane Reade by Walgreen’s” as my least favorite kludgey brand names.

How can Wonderland and other DeFi favorites offer such incredible interest rates? Short answer, they kind of… Can’t? To earn that juicy income, you must first convert your fiat ducats or stablecoins or bitcoins into a fast-depreciating hyperinflationary asset / token whose only hope of avoiding a death spiral is an infinite stream of new speculative money that can slap Band-Aids on the gaping wounds of inflationary collapse.

This excerpt from thismorningonchain.com explains it well:

How Wonderland Works

Wonderland famously averaged an 80,000% APY, paid in TIME tokens. The idea is that investors buy TIME tokens, which Wonderland mints. Wonderland then uses the investors’ funds to buy treasury assets. TIME's value is expected to fall over time, and the project's economics rely on a steady stream of new investors entering the ecosystem to keep TIME’s price from crashing.

Investors were wary of the projects' claims of high APY, but Wonderland's leadership promised to stabilize the token's price with TIME buybacks funded from the Wonderland treasury. Many Wonderland investors took this as evidence of a "price floor," and leveraged their assets accordingly.

Wonderland isn’t the only protocol running the hyperinflationary high-yielding currency strat (and no, I’m not talking about Argentina). Some others from

Oops! Wonderland, the anonymously-run, unregulated free money faucet also may have some sketchy ties.

Further reading: https://www.coindesk.com/policy/2021/12/05/olympus-dao-might-be-the-future-of-money-or-it-might-be-a-ponzi/

Walk towards the light

But enough about the darker, riskier corners of DeFi. There is a large new “digital income” industry developing as well, and it’s not to be confused with the scammy forms of DeFi that capture the headlines.

As crypto becomes its own parallel and leveraged financial universe, it will compete for investment dollars with the fractional reserve / fiat system. Moving money from a fiat system into the crypto system is expensive, so crypto investors don’t want to keep going back and forth between crypto and fiat. As the Constitutional DAO peeps found out (and as my personal experience confirms) crypto fees can often make Western Union look like a bargain.

But as more and more money pours into crypto, it’s not all just speculative cowboys chasing capital gains like ye olden days of 2014. Now, crypto HODLers include conservative investors who may not be seeking parabolic lotto-ticket gains. Their hopes are more modest: yields that don’t start with zero. These conservative participants are likely to be attracted by digital income products that are overcollateralized and safer than old-school Wild West DeFi protocols. Still, it will be a while before everyone fully understands how this new hardly-regulated, highly-levered mutant financial system will behave under extreme stress.

Maybe it is resilient to shocks, or maybe not.

Will overcollateraliozation protect investors if there is some kind of Black Swan flash crash that sends BTC back to $2,500 in a nanosecond? Hard to say. I’m not predicting or expecting such a crash, but the highly-leveraged fiat system has shown itself to be extremely fragile under duress and so it’s reasonable to think the crypto system will experience points of failure here and there too.

The difference is that the government bails out the traditional system when it fails. Crypto investors will be on their own.

I don’t want to overstate the fragility or systemic risk in crypto, I’m just saying uninsured investments have different risk of ruin characteristics than insured ones.

Introduction to digital income

Inside the crypto ecosystem, there is massive supply and demand for liquidity, lending, and borrowing. Just like in the stock market, there are players who want to borrow crypto for short selling and other levered activities and thus there is a positive yield on most cryptocurrencies. The riskier the token, the more the yield, ceterus paribus, but even stodgy old bitcoin pays better than negative-yielding bonds or gold. As such, former TradFi experts are creating new products that offer enhanced “digital income” to investors.

Marcel Kasumovich, Head of Research at One River Digital, and a well-known and well-respected name in TradFi world, recently wrote an excellent piece called “Income problems with digital solutions.”

I am sharing it here with Marcel’s permission.

income problems with digital solutions

by Marcel Kasumovich, Head of Research, One River Digital

1/ Portfolios, we have a problem. U.S. household financial assets have risen to nearly 5-times nominal GDP in the Great Financial Inflation. So great is the financial inflation, households find themselves (perhaps unintentionally) with a whopping 49.2% allocation to cash, cash-equivalent assets, and bonds (Figure 1). This comes at a time when macro policies are resolutely committed to multi-generational financial repression. For all the hawkish hype, bond markets are convinced that the next easing cycle will come in 2023 and that long-term policy rates will remain well below inflation. This is strongly counter to Fed guidance. We see no historical precedent.

Figure 1: Great Financial Inflation: Large Bond Holdings

Source: Federal Reserve Board. St. Louis Federal Reserve. One River Digital Calculations. Provided for illustrative purposes only.

2/ So, financial markets are telling us that nearly 50% of household assets are expected to lose money in real terms in the decades ahead. It is not just a U.S.-asset problem – shorter-term real yields are a global phenomenon (Figure 2). The Great Financial Inflation has masked the misallocation – long gone are the days of diversification. A 60-40% equity-bond portfolio returned 15% last year with a coincident rise in equity and bond valuations. Bonds have taken on equity-like return characteristics – the 60-40% portfolio is unbalanced. No doubt, the drawdown in 60-40% portfolios to start this year was on par with crisis periods – we were only missing the crisis – with equities and bonds both sharply retracing in January.

Figure 2: Problem: Low Yields, Inflation Taxing Bond Portfolios

Source: Bloomberg. One River Digital Calculations as of February 9, 2022. MKT L-T FED DOT is the 5y5y OIS forward to imply the long-term Federal funds policy rate. L-T inflation is 5y5y forward inflation..

3/ Are digital assets a potential solution to balance portfolio risk? Yes. But the solution has a more subtle first step: yield. Directional exposure to bitcoin and the One River Digital Core Index seeks to offer diversification properties over the course of the market cycle. However, shorter-term cyclical correlations are still quite high. Daily bitcoin returns year-to-date have a 53% correlation to US equity returns and a 36% correlation to US fixed income. Not all investors are searching for more risk, slowing the institutional adoption to directional digital asset exposure. Ethereum’s migration to proof of stake will mark a milestone, transforming ether into a bond-like asset. But even then, the yield from staking is low relative to the ether’s volatility.

4/ A more natural first step for some investors is to focus on yield derived from the digital ecosystem. Ideally, a yield investment would avoid any directional exposure and offer an income-like cashflow that is familiar to institutional investors. It would bring digital assets to investment committees in a low-risk manner, a more natural fit for their mandates (What’s Taking So Long? here). It was missing – an uncorrelated, low-risk, liquid yield fund without direct digital asset exposure. So, we built it: the One River Digital Income Fund. The objective was clear – deliver a low-risk yield solution in the digital ecosystem. The lowest end of the risk spectrum is the natural starting point – risk can be added alongside the evolution of investor appetites easily enough.

5/ Digital Income is a short-term yield fund. The Fund seeks to generate yield by providing a U.S. dollar loan to high-quality borrowers in the digital ecosystem. The loan’s safety is achieved by over-collateralizing the loan through high-quality liquid digital assets, initially only bitcoin. The Fund does not take possession of the bitcoin and thus is not a money transmitter, an important consideration in the context of future regulation. Instead, the liquid collateral is held by a third party with conditions on when collateral can be liquidated (Figure 3). Our process selects known, researched, and regulated counterparties. Investors are granted the added security by over-collateralization of a liquid asset with 24-hour margining, 365 days a year.

Figure 3: Solution: Digital Income, Lowest Risk Strategy in Digital Ecosystem

Source: One River Digital. This chart is provided for informational purposes only and represents a simplified description. The above investment strategy may differ from what is stated above at One River's discretion.

Here are the four most common questions on Digital Income:

6/ What are the risks to the structure? Short answer – negligible. Digital Income builds layers of protection. The over-collateralization means that a default scenario is recognized well before collateral values breach the par value of a loan. This negates counterparty risk. Digital Income also allows for U.S. dollar collateral, which can be used to buffer a cascading decline in the price of bitcoin. Further, the loan has recourse beyond the collateral. These measures are designed to add safety. Not surprisingly, our estimates of the “risk premium” needed to compensate for collateral risk is comfortably less than ten basis points. The yield is not compensating lenders for a known risk premium. Instead, Digital Income will seek to provide income to lenders for intermediating activity in the digital ecosystem. And we believe there is a shortage of high-quality lenders doing so.

7/ Second, where does the yield come from? Demand for capital in the digital ecosystem is robust, alongside high expected asset returns. This is the natural flipside of high asset volatility. In the early phase of lending growth, retail capital, such as yield-bearing digital deposits, was sufficient. However, as the system has matured, growth in loan demand has increased through digital banking partners, high net worth individuals, corporations, hedge funds, and family offices. Active loans for Genesis Global Trading, for instance, are approaching $10 billion, an increase from less than $1 billion at the start of last year (Figure 4). Rapid and broadening growth in digital assets will require substantial debt capital, including attractive, low-risk rates for institutional investors.

Figure 4: Market Demand, Shortage of High-Quality Lenders

Source: One River Digital. Provided for illustrative purposes only.

8/ What is the right benchmark to compare Digital Income? Digital Income is a quarterly fund and will be compared to cash-equivalents such as the Bloomberg 1-to-3-month U.S. Treasury bill total return index. We anticipate Digital Income yields to be in the 4-12% range, varying pro-cyclically with the demand for capital. A rise in digital asset prices raises expected returns and the interest rates paid by the borrower, even with collateralization. Rates are driven by demand. However, it is important to value Digital Income relative to other benchmarks. One way is to infer unsecured funding rates from publicly traded digital asset companies. Five-year unsecured financing, inferred from one convertible bond, is running at ~4%, the low end of our expected range. Digital Income is secured and can still offer an attractive premium.

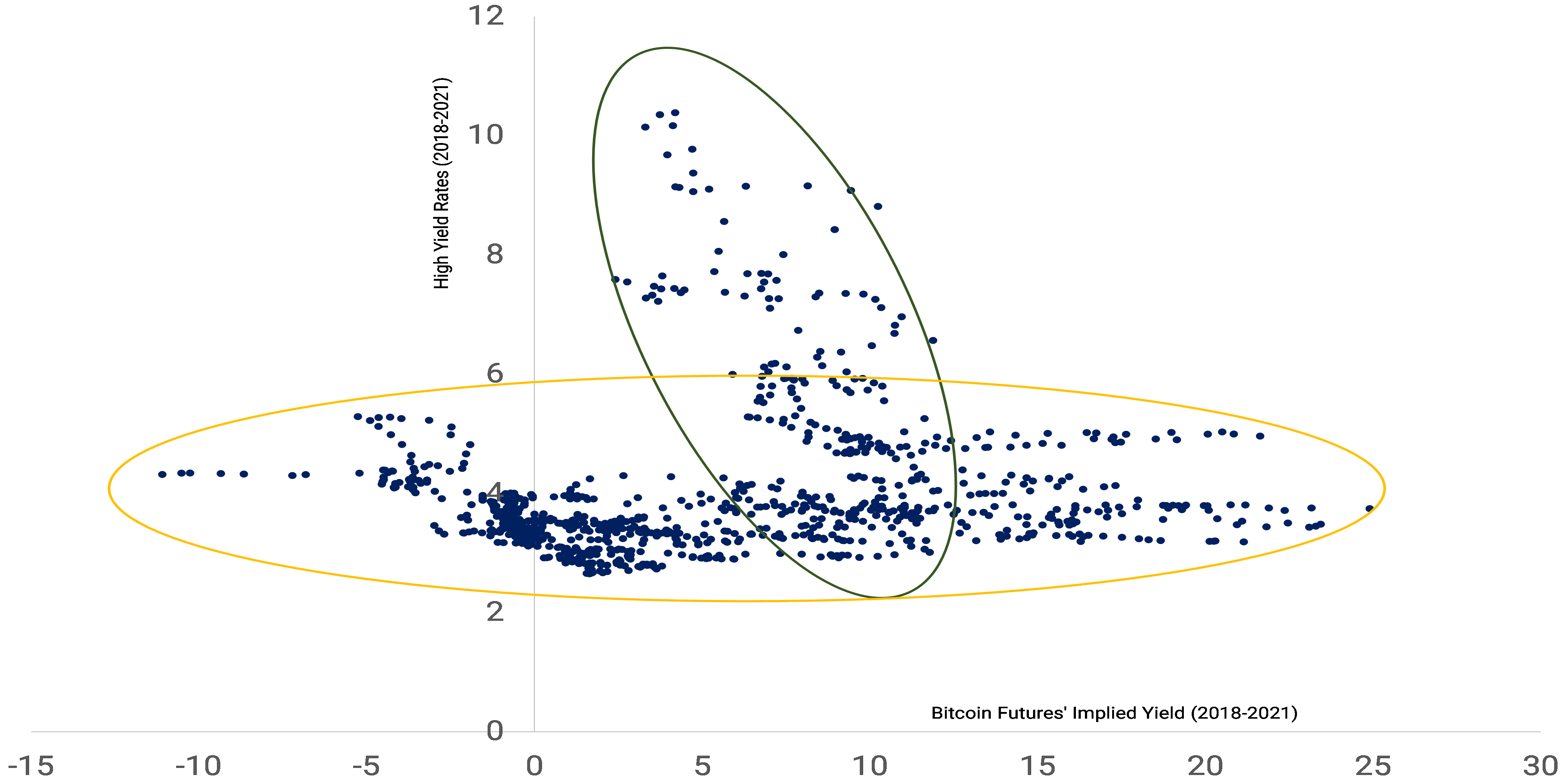

9/ How does Digital Income fit into a portfolio? This is a subtle benefit. Typically, credit and risk assets co-move. As equity asset prices decline, credit spreads widen. This is a mathematical truism of credit spreads– it is equivalent to being long a risk-free asset and short an equity put. But this is not how yields in digital assets behave. Figure 5 illustrates the implied yield in bitcoin futures against high-yield corporate borrowing costs. Most of the time, there is no correlation. However, digital asset yields decline alongside the fall in the demand for borrowing in sell-off periods for risk assets and widening in credit spreads. Digital Income spreads are counter-cyclical, narrowing as asset prices decline. This behavior is more like a Treasury bill than credit.

Figure 5: How Do Spreads Behave? Opposite of Credit!

Source: Bloomberg. One River Digital Calculations. 2018 to 2021. The above graph demonstrates implied yield in bitcoin futures against high-yield corporate borrowing costs, both in percent. The bitcoin futures’ yield is a five-day rolling average of the daily annualized yield implied by the ratio of the one-month rolling bitcoin future to the spot bitcoin price. See important disclosures at the end of this article.

10/ The beginning is a good place to start. That is precisely what we are doing with Digital Income – we are defining the lowest risk point of the digital asset yield curve. Doug Wilson, the portfolio manager, executed our first loans this week with research and operational tools in place. We believe that this will be a comfortable step into the digital ecosystem for institutional investors. And it will also be a natural point from which to migrate out the risk spectrum, lowering collateralization rates to enhance yields and moving into credit provision through bitcoin bond-like structures. Bonds are a problem, and we believe Digital Income is a solution.

Conclusion

Today I pointed to two ends of the DeFi/digital income/yield farming spectrum.

We will continue to see rapid innovation in this area as financial repression cripples savers in the fiat system. The trick is to properly quantify the risk you are taking as you pursue max allowable APY. The trick is to properly weigh the return on capital vs. the return of capital.

Those firms that create competitive digital income products that are truly safe, or at least safe enough, are about to attract massive inflows over the next five years.

The One River product is not alone. There are many others at various points on the respectability and risk/reward spectrum. Here’s another participant in the digital income space that is making some noise of late.

Seems logical enough, but this statement on their website …

… reminds me of the infamous Bernanke interview before the housing bubble burst.

When I read “have never defaulted”, my brain hears a whisper:

So far.

I’m not critiquing or endorsing any products here. I just think the rise of digital income as a rebranded, safer subset of DeFi is interesting and important.

So there you go… DeFi for the TradFi Guy. That concludes MTC #14.

Thank you for reading!

If you like dark fiction and don’t mind a bit of implied violence and swearing, check out the secret but not so secret MTC #13: Unlucky. I didn’t send it by email because I think many people will dislike it. Read at your own risk.

bd

The big driver of crypto these days is global macro.

If you want to be in the know on global macro, sign up for my daily.

Macro is my real job. MTC is just for fun.